ABC analysis is a method used in inventory management and business decision-making to categorize items or products into three categories based on their importance or value to the organization. The ranking or categorization of inventory items is dependent on their consumption value regarding material and distribution management.

The purpose of ABC analysis is to help organizations allocate their resources more efficiently by focusing their efforts and resources on managing the most critical and valuable items (Category A) while requiring fewer resources for the less important ones (Category C). This approach allows for better inventory control, reduced carrying costs, and improved inventory turnover.

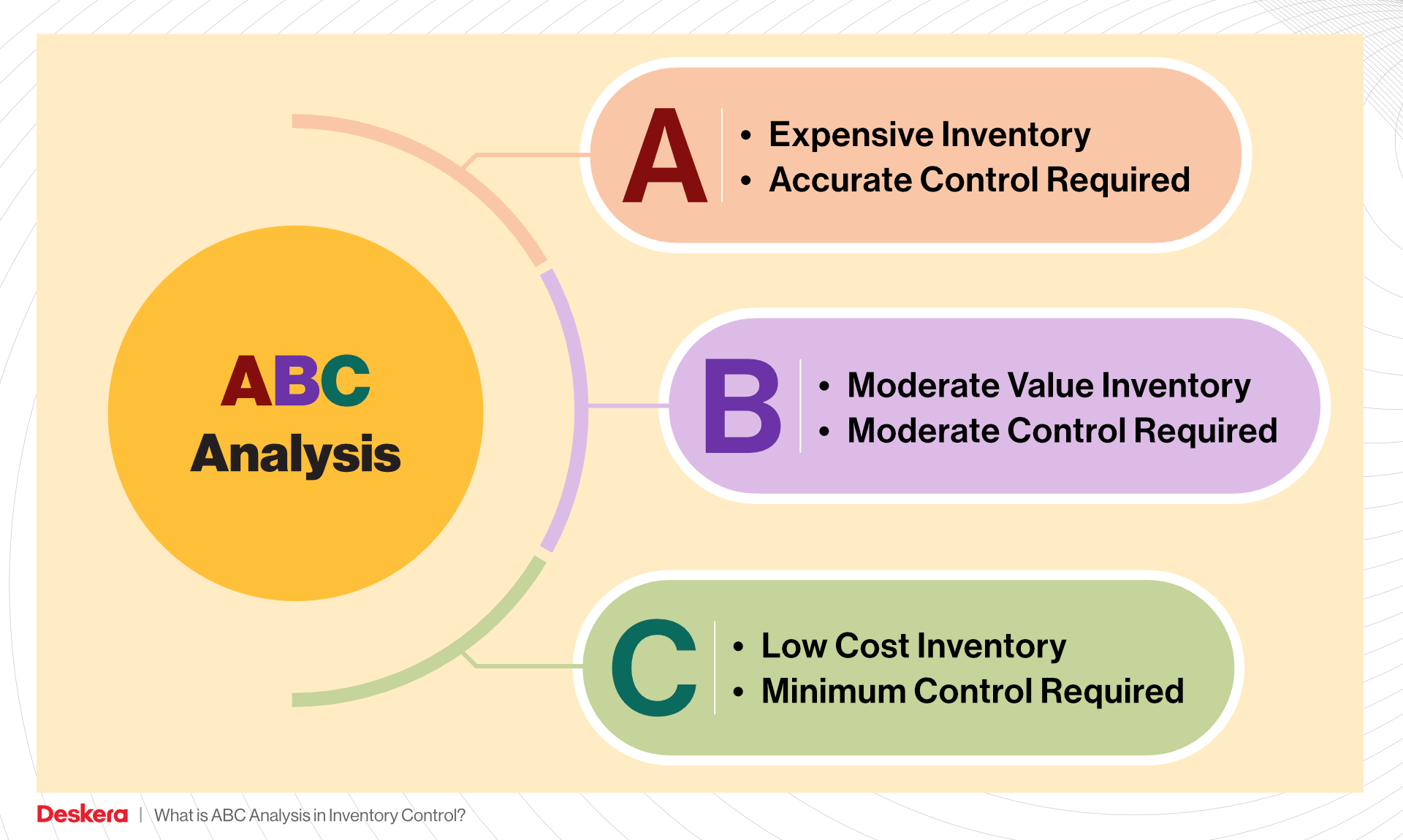

ABC Method

The ABC method is a widely used inventory classification technique that groups products into three categories—A, B, and C—based on their business value and contribution to overall performance. By segmenting inventory according to importance, companies can prioritize resources, optimize stock management, and focus their attention on the items that have the greatest impact on revenue and operational efficiency.

The three categories help businesses determine different inventory control strategies, forecasting approaches, and replenishment policies for each group of products.

Category A

These are the most valuable and important products of a company. They typically represent a small percentage of the total items but contribute to a significant portion of the overall value or revenue. Managing these items effectively is crucial to the business’s success, as these items produce the greatest output with a small input. Category A commodities often require closer attention, tighter control, and more frequent monitoring.

Category B

Category B items are moderately important. They have a moderate impact on the overall value and are neither as critical as Category A items nor as insignificant as Category C items. These items are managed with a moderate level of attention, and inventory policies for B-Items may involve less frequent review and replenishment than A-Items. However, certain products may turn into Category A items with some effort, as B-items contain lots of potential.

Category C

These are the least valuable or important items in the inventory, often constituting a large portion of the total number of items but contributing minimally to the overall value or revenue. C-Items are typically low-cost, low-value, or slow-moving items. These may be hundreds of small transactions that don’t individually contribute a significant amount to revenue. Category C items are managed with the least amount of attention.

What is ABC analysis?

ABC analysis is a method of inventory management that looks at organising and managing large amounts and ranges of inventories. It has been seen to be adopted and adapted across various industries, quickly becoming a crucial method of inventory management in the business world. It is oftentimes used in conjunction with other management and organisation techniques and software systems.

ABC analysis is based on the Pareto Principle, you may be familiar with it as the 80/20 rule. The main idea of this Pareto principle is that most economic productivity comes from only a small part of the economy. The principle underlines the unequal relationship between input.

ABC analysis divides an organization’s on-hand inventory into three classes based upon their value. This inventory categorization method divides items into A, B and C categories. A is the category of the most valuable items, with B and C ranking next. The main goal of this analysis is to ensure the manager focuses the attention on the critical few A-items rather than many trivial C-items. Inventory optimization is crucial in keeping the supply chain costs under control.

Categorizing inventory items based on their relevance is fundamental for an ABC inventory analysis system. Organizations can allocate resources more effectively due to focusing attention, time, and capital on Category A items. Similarly, this enables cost control as Category A items receive closer scrutiny and investment relative to less critical Category B and C items, which will have lower carrying costs and less stringent controls. By categorizing items, organizations can focus on inventory optimization by having stricter inventory management techniques for Category A items to reduce carrying costs and stockouts, whilst saving costs by having more relaxed policies for Category B and C items.

How Does ABC Analysis Work?

ABC Analysis is broken down into 3 specific categories, namely, A, B, and, C. These categories are ordered according to historical sales data, cost, and usage. While the criteria for each category may vary from organization to organization, the above factors largely inform what will be found in each category.

Let us dissect what may occur in each category:

Category A:

- High Importance: These items are the most important and valuable inventory items, contributing a significant portion of value of the organization.

- High Value: As described above, these items tend to have a high monetary value or reliable profit generators.

- Close Monitoring: Category A items are closely monitored and managed as they tend to require frequent reviews and replenishments to ensure constant availability.

- Tight Control: Requiring tighter controls around their inventory policies, much focus is placed on Category A items in order to mitigate the inventory risk of stockouts.

Examples of Category A items would include best-selling products, high-margin items, and components that are critical for production.

Category B:

- Moderate Importance: Scaling down from the previous category, Category B items have a moderate impact on the overall value of the organization.

- Moderate Value: While they are seen as valuable, Category B contribute less profits than Category A items.

- Moderate Monitoring: These items are managed with moderate attention, but their review and replenishment may be less frequent than Category A items.

- Balanced Control: Category B inventory items have balanced inventory policies to maintain adequate stock levels without overinvestment.

Examples of Category B inventory items are mid-range products and production components that have moderate importance in the production process.

Category C:

- Low Importance: These items are the least valuable, as they contribute a minimal amount of overall value. They might, however, occur in large amounts.

- Low Value: Typically low-cost, low-value, or slow-moving items, thus Category C items are less vital to the financial performance of the organization.

- Low Monitoring: The review and replenishment of Category C items may be infrequent, as these items are managed with the least amount of attention.

- Minimal Control: The risk of stockouts of overstocking is relatively low for Category C items, and inventory policies involved minimal control for these items.

Low-demand items, cheap consumables, and spare parts are examples of Category C items.

ABC analysis is extensively used in supply chain management and inventory systems. One of the best ways to decrease working capital and respective carrying costs is by performing an in-depth analysis of inventory. If the levels of inventory are not regulated accordingly, you might always have either too much or too little stock in your warehouses. This could lead to a number of issues in the future. Performing an ABC analysis helps to identify which items should be in stock to satisfy the customer demand with the least additional costs for the company. It is evident that ABC analysis offers the following two main benefits – the first being better control over high-value inventory, and the second, efficient use of stock management resources. These benefits bring along multiplied advantages of minimized costs and losses, and better organised production.

Why use this analysis? What benefits can it bring?

ABC analysis of inventory has many benefits. Its main goal is to improve your ability to understand large and complex data by breaking it into segments and prioritizing. Any data is easier to analyze if it is broken down into segments. This brings out specific issues within segments and helps to prioritize among different segments accurately. With a clear picture in mind, it is much easier to come up with a plan of action, without wasting much of the company’s resources.

ABC analysis is extensively used in supply chain management and inventory systems. This is one of the best ways to decrease working capital and carrying costs by analyzing the inventory in depth. If the levels of inventory are not regulated accordingly, you might always have either too much or too little stock in your warehouses. This could lead to a number of issues in the future. Performing an ABC analysis helps to identify which items should be in stock to satisfy the customer demand with the least additional costs for the company. With this in mind, you can see that ABC analysis offers the following two main benefits:

- Better control over high-value inventory, which results in minimized costs and losses, and

- Efficient use of stock management resources, which helps to organize the production or re-sale more efficiently.

How to interpret the analysis data?

Of course, conducting an ABC analysis of inventory won’t be of any use, unless you interpret the gathered data properly. Here are a couple of tips concerning your findings to actually make savings based on the results of the ABC calculations. Once you’ve classified the inventory items into three categories, have a closer look at your final data. Review how the inventory in each category is managed. Policies based on ABC analysis might include investing more resources in certain categories compared to others. As a rule of thumb, not all categories should be treated the same, otherwise, it would make no sense to categorize items in the first place.

No differentiation among categories would lead to inefficient and needlessly expensive inventory management. This is why you should adapt your inventory policies to each category according to the data collected by the ABC analysis. For instance, some items of value, such as A-category items, could require more time for discussion and negotiation. This could get you the best quality to price ratio. As for items of lower importance, such as C-category items, you may not need excessive and timely discussions.

Same goes for purchase and re-stocking frequency. Some high demand and high value A-category items may need restocking more often than items from C category with much lower demand. The key here is to make sure you’re allocating most of the attention to those items that have the highest conceivable savings. This is one of the main reasons to incorporate ABC analysis: to save more.

The second important factor you need to pay attention to when going through the data are indicators of potential. Have a closer look at the items in each category. Are there any items that have the potential to have a higher value or a higher demand, that you should move to a higher category? This might be revenue that you’re leaving on the table.

On the other hand, you should also look out for items in the highest-ranked category (A) to which you may be allocating too much attention or credit. Some of these items might not exactly be bringing as much value to your business as you would think. If so, you should consider to filter these out the category and move them accordingly. You should also consider inputting the extra resources and time wasted on such category A items on other items. These could be category B or C items, which have big potential. Perhaps they could transform into category A items in terms of their value with a little more input or minor adjustments.

Implementing ABC Analysis

Conducting an effective ABC analysis involves a systematic, step-by-step approach to categorizing items based on their importance or value to the organization. The approach can be broken down into the following steps:

- Data Collection: Gather relevant data for each item of inventory that your company wishes to analyse. Date to be looked at can include sales data, cost data, or usage data. Each inventory item should have a unique identifier, with value and monetary-based criteria that will be used to categorise them.

- Calculation of the Criteria: Once the items and criteria have been established, calculate the chosen criteria for each item accordingly. For example, if you’re using monetary value, calculate the total sales value for each item over the specified time frame. From these findings, rank the items in descending order, with the item of the highest value topping the list. The categories can then be defined, and each item can be assigned to the category of criteria they best suit.

- Documentation: Document the results of your ABC analysis: criteria used, the thresholds of each category, and the items assigned to each category. Inventory strategies can be created based on these results. Regular review is important for constant, updated improvement of the ABC analysis inventory management system.

- Integration with Software: In our modern world, it is almost a necessity to apply your inventory management techniques alongside software that can automate the categorization process, just like Intuendi! These technologies can help you implement and track the strategies for each category more efficiently.

ABC Analysis Across Different Industries

Let’s see how different sectors use ABC analysis.

Retail Sector: In retail, seasonal variations can significantly impact sales. Consider incorporating seasonality factors into the analysis to ensure that products are categorized appropriately. Trends and changing consumer preferences may also impact the analysis. Products may move between categories as consumer demand fluctuates.

Manufacturing and Production: Production lead times and supply chain disruptions can have a substantial impact in a manufacturing operation. Consider factoring in lead times when determining inventory policies for Category A items. Furthermore, it is recommended to consider the impact of production bottlenecks and the availability of key components in the categorization process of materials or products.

E-commerce and Technology: E-commerce companies need to consider the fast-paced nature of the industry, where new products and trends emerge quickly. Thus, regular updates and revisions to the categorization of items are critical. Technological obsolescence can render items in categories outdated. One should factor in the rapid advancements and short product lifecycles of certain items when performing the analysis.

Service Industries: In service-oriented businesses, consider the availability and utilization of resources, such as human resources, equipment, or office space, and categorize them based on their importance and utilization. These considerations emphasize the importance of tailoring ABC analysis to the unique characteristics of each industry or sector. It’s crucial to adapt the analysis to specific challenges, risks, and opportunities that are prevalent in relevant sectors to ensure that resource allocation and inventory management strategies are both effective and contextually relevant.

Optimizing Inventory Management Using ABC Analysis

As previously stated ABC analysis can be used to optimize inventory management. Lets take a deep dive into how each category contributes to inventory management

Category A Items: Because of their importance and value in a company, Category A items require real-time tracking systems. Keeping a close eye on their whereabouts is paramount. It is equally important that safety stock levels, calculated based on demand variability and lead times, are maintained in order to prevent Category A stockouts. Above this, Category A items should have shorter reorder points to ensure they are replenished more frequently. Managing the supply of Category A items involves selecting reliable suppliers and fostering strong relationships with them. How Category A items are forecasted is also of utmost importance. Sophisticated demand forecasting techniques should be allocated toward the forecasting of these items to ensure a prepared manufacturing and supply chain.

Category B Items: Category B items, with a moderate level of importance, should also be monitored at a reasonable frequency, but just not as intensively as A-Items. A balanced approach to inventory control for B-Items should be used – management techniques that are neither too conservative nor too risky. It is recommended to maintain good relationships with suppliers of Category B items, but these may not need the same level of exclusivity or collaboration as with suppliers of Category A items. The organization should focus on improving inventory turnover rates for B-Items by setting inventory policies that allow for a healthy balance between supply and demand. Companies should also consider demand variability and seasonality in their inventory policies for B-Items, adjusting reorder points and order quantities accordingly.

Category C items: Category C items are of the lowest importance out of the 3 categories, and their monitoring can be less frequent. Businesses should review them periodically, but with longer intervals than the previous 2 categories. Minimal control measures for C-Items should be used, and bulk ordering strategies are recommended. Supplier agreements should only be leveraged for bulk purchases. If you use the ABC analysis techniques, you should be aware of the potential obsolescence of C-items and should have a clear strategy for disposing of outdated stock. The costs associated with monitoring and managing C-items can be minimized, as they are less critical to overall operations.

These strategies can be adjusted based on the specific needs and characteristics of an industry or business. Regular reviews and adjustments to the ABC classification process and corresponding strategies are essential to ensure ongoing efficiency and effectiveness in resource allocation and inventory management.

Challenges and Potential Limitations of ABC Analysis

The main problem with policies based on ABC analysis is that they are not compliant with GAAP (Generally Accepted Accounting Principles) requirements. It’s a common set of accounting standards, principles, procedures and rules used by companies for complying financial statements. ABC calculations are not compliant to GAAP due to several reasons.

One of the major reasons is that ABC systems conflict with GAAP when it comes to assigning manufacturing costs to products. Under the ABC system, not all manufacturing costs are assigned to products, unlike GAAP. The logic behind this approach is that expenses such as rent, security, heating, and other organization sustaining costs will be incurred regardless of production levels. So, ABC systems do not assign such costs to specific products. If a certain cost does not depend on the production volume, then such cost is not really relevant to decision-making. From the managerial perspective this approach may make sense, nonetheless, it is still considered a violation of GAAP.

Another reason why ABC systems are not compatible with GAAP, is the exact opposite of the first one. Under ABC systems some specific non-manufacturing costs may be assigned to a product, which is not allowed under GAAP. The logic behind this is the same. If a cost is relevant to the product, it should be included in the product cost, regardless of the fact that these could be non-manufacturing costs.

As a result, since ABC system conflicts with GAAP, an additional costing system will be required besides the ABC method to comply with GAAP.

At some point supply chain managers will face another problem with ABC analysis. It might be challenging to decide in which category to fit an item in. Due to the rise of e-commerce and social media trends may dictate a sudden spike in demand for some items. Such items could initially seem like outliers from a lower category and be unpredictable. When the demand of such items raises overnight, the value raises with it. This means that the item will have to be moved to a higher category in the ABC system. So, supply chain managers would have two options. First one is to constantly monitor and update the classification. The second one would be to try predicting such often unpredictable demand spikes ahead of time, before even categorizing an item.

Another important issue that partially results from the previous two, is that the ABC system will require more resources to maintain, unlike traditional costing systems. Due to their high value and importance class A items must be analyzed constantly to determine whether the category still consists of high-priority items at any given time. Any items that no longer hold high value and are not in demand have to be moved to another category. Constant updates and monitoring will require more data collection and measurement. This can be quite costly.

Despite some disadvantages, ABC analysis of inventory is a great way to gather and use relevant data. This data could be useful in reducing excess costs and generating more profits. For best results, however, it is also important to constantly monitor the categories. You must also update them according to changing demand levels in the market and wisely organize your inventory management with an intelligent demand planning software by tailoring your approach to each category.

If you found this interesting take a look at this case study where a multi-dimensional ABC analysis applied to a growing business helped maintain a lean inventory while supporting growth: